Market structures

Perfect competition model

- Perfect information

- Homogeneous goods

- Perfect mobility

- Price-takers

- Large number of firms

Monopolistic competition

- Perfect information

- Homogeneous goods

- Perfect mobility

- Price-takers

- Large number of firms

Oligopoly

- Perfect information

- Homogeneous goods

- Perfect mobility

- Price-takers

- Small number of firms

Monopoly

- Perfect information

- Homogeneous goods

- Perfect mobility

- Price-takers

- One firm

Conclusion

Market equilibrium

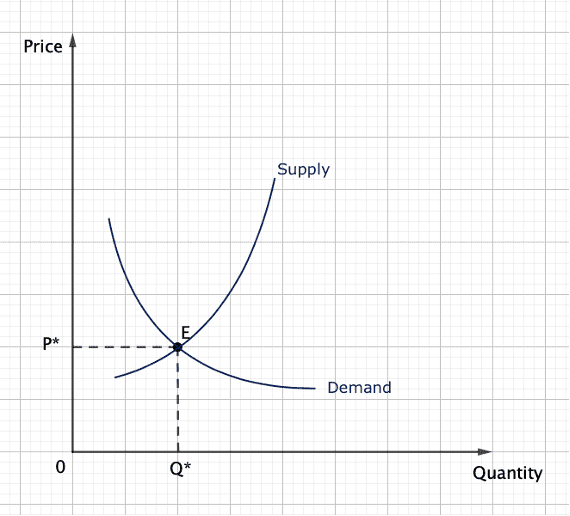

Equilibrium

Equilibrium is attained at the price at which quantities demanded and supplied are equal. In other words, the equilibrium is the intersection point of demand and supply curves. Its coordinates are, most of the time, denoted (Q*, P*) where Q* is the equilibrium quantity and P* the equilibrium price.

Change in equilibrium

| Price | Quantity | |

| Demand increases | Increases | Increases |

| Demand decreases | Decreases | Decreases |

| Supply increases | Decreases | Increases |

| Supply decreases | Increases | Decreases |

| Supply increases | Supply decreases | |

| Demand increases | Price ? Quantity increases |

Price increases |

| Demand decreases | Price decreases Quantity ? |

Price ? Quantity decreases |

Key words

Shortage: when quantity supplied < quantity demanded

Surplus: when quantity supplied > quantity demanded

Disequilibrium: when quantity supplied ≠ quantity demanded (either a shortage or a surplus)

Equilibrium: when quantity supplied = quantity demanded